The latest report from Centrum Sugar Industry sheds light on the current state of the sugar sector in India, indicating a mixed bag of trends with potential implications for the market. As of January 31, 2024, state-wise crushing data for SSY24 reveals a narrowing year-on-year difference in sugar production, yet the overall outlook remains negative, primarily due to factors such as decreased production in key states and government policy shifts affecting ethanol volumes.

Sugarcane Crushing Trends

Sugarcane crushing activity has witnessed a 4 percent decrease compared to the previous year, marking an improvement from the 7 percent reduction observed earlier. This decline is primarily attributed to Maharashtra, which experienced a 10 percent drop, and Karnataka, with a more moderate 3 percent decrease. The reduction in crushing activity correlates with a lower count of operational mills, particularly in Karnataka, where the number has fallen from 279 to 272. However, Uttar Pradesh has shown resilience in this regard, with a 3.7 percent increase in sugarcane crushing, aligning with a modest rise in operational mills compared to the previous season.

Impact on Sugar Production

The decrease in sugarcane crushing has translated into a decrease in sugar production, totaling 18.7 million metric tons (MMT) compared to 19.3 MMT during the same period in the previous year. Notably, Uttar Pradesh stands out with a remarkable 13.3 percent increase in sugar production, reaching 5.8 MMT, coupled with a recovery rate of 10.1 percent, up from 9.2 percent in the previous season.

Expectations for SSY24

Despite the fluctuations observed, industry projections suggest a downward revision in sugar production for SSY24, estimated at approximately 31.7 MMT, down from 33 MMT in SSY23. This revision is primarily attributed to lower sugar production in Maharashtra and Karnataka, driven by reduced yields and recovery rates.

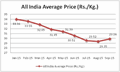

While domestic sugar prices have remained stable in recent months, the overall outlook for the sector remains pessimistic. Recent notifications from the centre, particularly those impacting ethanol volumes and pricing, have contributed to this sentiment. The cancellation of direct route contracts and suspension of BH in future tenders, alongside upward revisions in CH ethanol pricing, are expected to encourage higher sugar production, thus exerting downward pressure on sugar prices.

Consequently, industry experts caution against complacency and emphasize the need for a cautious approach amidst evolving market dynamics.